East Side Games (TSX:EAGR) Q2 2024 update

East Side Games Group reported their Q2 2024 Results yesterday night

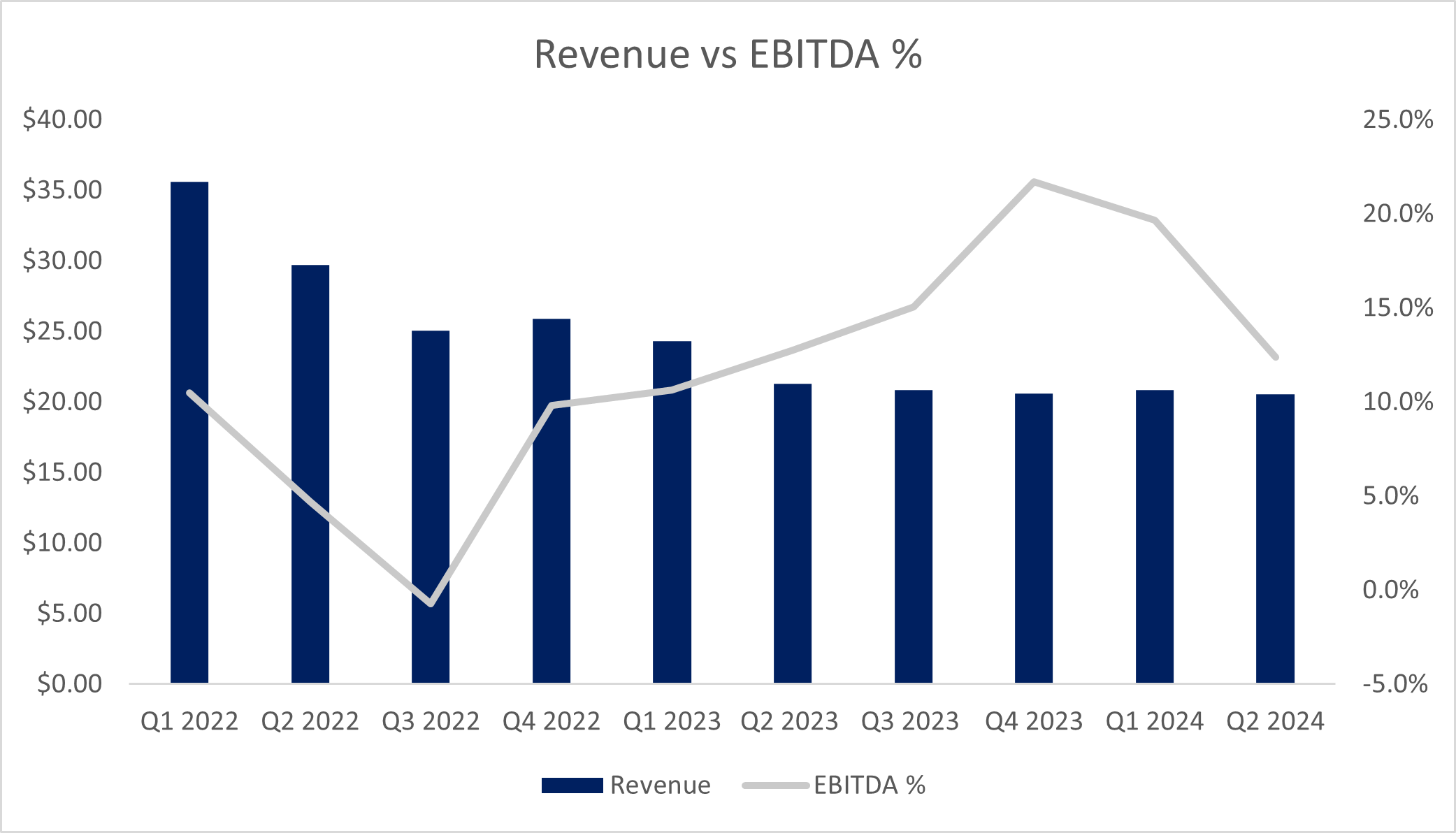

Revenue was down 3.5% YoY; I was looking for growth. Margins dropped to 12.4% QoQ (EBITDA went from 4m in Q1 to 2.5m in Q2) on the back of significant UA spend driven by their investment in their new GameKit category, Match-3. These investments are expected to pay-off in the coming quarters as they continue to scale Bud Farm: Munchie Match, Cheech & Chong and recently launched Power Rangers. Bear in mind that Q2 is a seasonally weak quarter.

In vacuum, the quarter seems to be a major step-down from Q1, but this is primarily due to investment timing. When factoring in UA spend on a newly created category + the roll-out of multiple games, it’s understandable to see a dip in margins near-term with the associated payback coming in later (retain customers first, then monetize). This also likely explains the mismatch between recent download trends and revenue trend.

Meanwhile, the continues to throw-off significant amount of FCF with FCF ex-working capital sitting at 5.3m for the first half of the year and 2.3m for Q2. At 0.90c/share, the stock is trading at a 15% normalized FCF yield.

The commentary in the press release and on the call were quite bullish and there were a few incremental points:

The company is targeting $10m of cash by EOY net of buybacks, which IMO could be higher if working capital swings the other way.

As I outlined in my initial write-up, the company is working on a new RuPaul game which they think can be a game changer for the company, especially given the success of the initial one

Power Rangers is performing better than expected and is generating over $1m in revenue per quarter one week into the launch - the company will reinvest all of the revenue into user acquisition in the near-term (which likely continue to depress margin).

Company will launch a new match game by EOY (likely the Queer Eye based match game) and another one early 2025 (RuPaul).

Bud Farm: Munchie Match saw its average revenue grow by 50% and the new Cheech & Chong match game is performing even better than the Bud Farm: Munchie Match game.

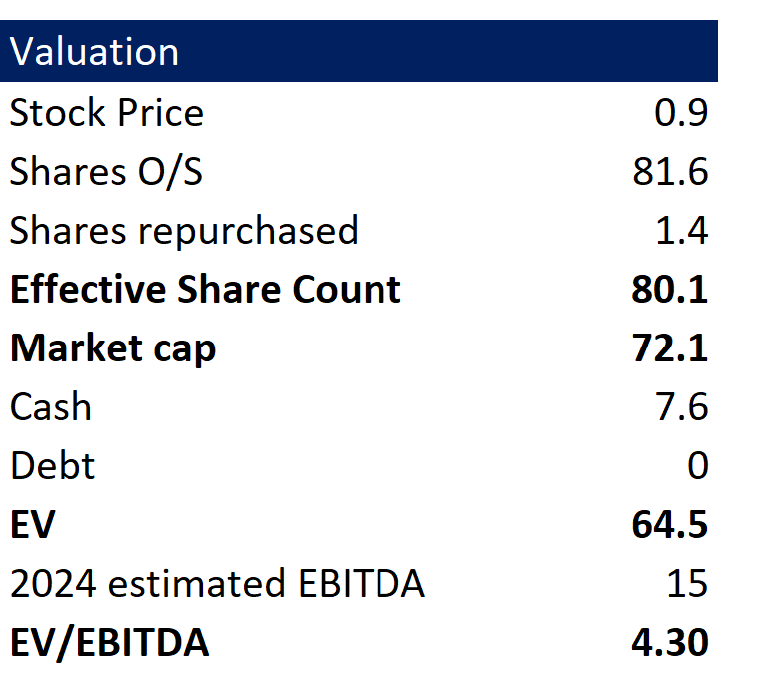

Valuation remains undemanding even with the stock being up 20% since my last substack post:

Conclusion

EAGR continues to be quite compelling trading <4.5x EBITDA on 2024’s number. the difference between my expectations relative to to the results seem to be all tied to the timing mismatch between UA spend and the future benefit the company will reap from it.

If the games (especially the new RuPaul) gain any traction, EBITDA could be well above $20m next year. Meanwhile, the company is piling up cash and returning cash to shareholders in the form of buybacks. My target price remains unchanged, and think the stock is worth $1.50

Any updated thoughts here? Big volume dump today out of nowhere so if it's just forced seller perhaps a great entry opportunity. Just too bad their NCIB is limited to a pitiful amount of shares per day.